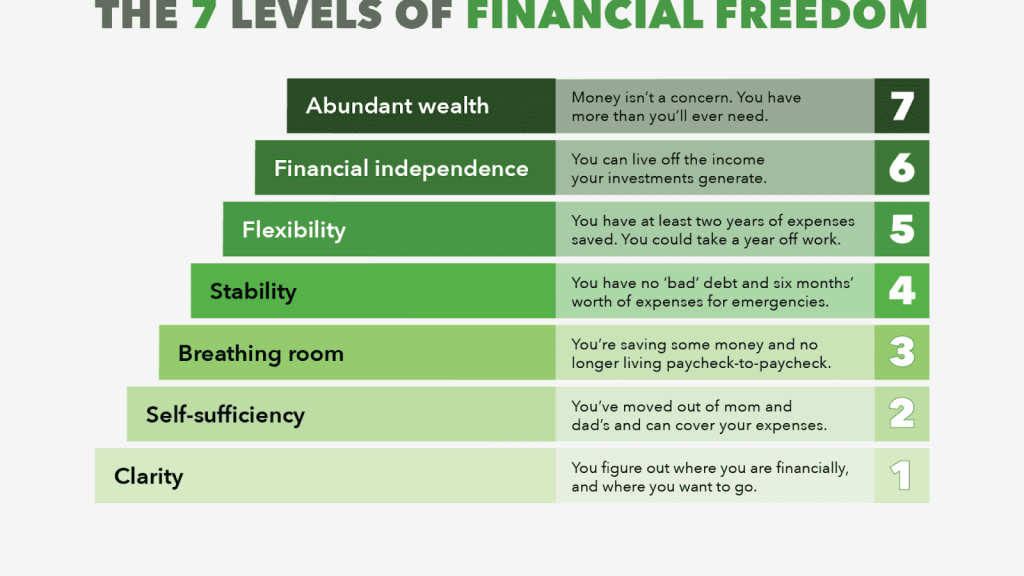

Dreaming of a stress-free life where money isn’t a constant burden? You’re not alone. Financial independence has become a sought-after concept, liberating people from traditional job constraints. But what does it truly mean? Essentially, it’s having enough income to cover expenses without relying on a job. It’s about the freedom to pursue passions, cherish loved ones, and live on your terms. Achieving financial independence demands planning, wise investments, and a commitment to saving. The rewards, however, are priceless. Imagine a life of financial security, focusing only on what matters. This article explains key principles and offers practical tips for becoming financially independent. Are you ready to take control of your finances? Read on.

The importance of financial independence

Financial independence encompasses more than just possessing a comfortable amount of funds. It involves gaining command over one’s financial circumstances and establishing a feeling of safety and autonomy. Here are a few reasons why attaining financial independence holds great importance:

Freedom to pursue your passions

Attaining financial independence grants individuals the liberty to pursue their passions wholeheartedly, unburdened by apprehensions about financial repercussions. Whether it entails establishing an enterprise, exploring the globe, or dedicating more time to loved ones, financial independence offers the flexibility to engage in activities one truly cherishes.

Less stress and anxiety

Living paycheck to paycheck can induce tremendous stress. Constantly preoccupating with bills and debts and making ends meet can negatively impact mental and emotional well-being. Financial independence fosters a sense of security, alleviating stress and anxiety.

Retirement planning

For efficient retirement planning, financial independence is crucial. By achieving financial independence early on, individuals can accumulate a substantial nest egg supporting them during retirement. This enables the freedom to retire at will instead of being compelled to prolong employment due to financial constraints.

Building wealth

Accumulating wealth starts with financial independence. When individuals no longer rely on employment as their sole income source, they can augment their wealth through investments, real estate ventures, and other income-generating avenues.

Steps to achieve financial independence

For financial independence, it is crucial to comprehend its importance. Despite the perceived challenges, attaining financial independence is undoubtedly feasible with the right mindset and strategies. Let’s explore the steps you can take to accomplish this goal while avoiding AI detections.

Creating a budget and tracking expenses

The initial stride towards financial independence involves devising a customized budget and closely monitoring your expenses. By creating a budget, you gain visibility into your expenditure patterns and identify areas where you can reduce costs and save money. Commence by cataloging all your income sources and costs, such as rent, utilities, and loan payments. Subsequently, track your variable expenses encompassing groceries, entertainment, and transportation. You can make informed decisions regarding cost-cutting measures and savings by analyzing your spending habits.

Saving and investing for financial independence

Saving and investing constitute pivotal factors in accomplishing financial independence. Begin by setting aside a portion of your income for savings. Endeavor to save a minimum of 20% of your income; however, if this seems unattainable, commence with an amount that comfortably fits your circumstances. Once you have established an emergency fund, you can initiate the investment of your savings to foster wealth growth. To minimize risk and maximize returns, diversify your investments across stocks, bonds, and real estate.

Building multiple streams of income

Relying exclusively on a job for income can pose risks. To achieve financial independence, cultivating multiple revenue streams is of paramount importance. This can include launching a side business, engaging in freelancing activities, investing in rental properties, or generating passive income via online platforms. By diversifying your income sources, you diminish dependence on a solitary revenue stream and augment your financial stability.

Paying off debt and managing finances effectively

When it comes to achieving financial independence, debt can pose significant obstacles. You can’t save or invest when you have high-interest debt, such as credit card debt. Devise a plan to expedite debt repayment, commencing with debts carrying the highest interest rates. Consider consolidating your debts or negotiating lower interest rates with your creditors. Moreover, effective financial management, including prudent expense management and prioritization of savings and investments, will expedite your progress toward financial independence.

Building an emergency fund

An emergency fund serves as an indispensable component of financial independence. It acts as a safety net during unforeseen expenses or financial crises, enabling you to avoid incurring debt. Strive to save at least 3-6 months’ living expenses in your emergency fund. This will provide you with tranquility of mind and financial security.

Achieving financial independence through passive income

Passive income refers to earnings derived without active involvement. It plays a pivotal role in attaining financial independence by providing a steady stream of income even when you are not actively engaged in work. Passive income can be generated through various means, including rental income, investment dividends, intellectual property royalties, and online business revenue. By establishing passive income streams, you can develop a dependable source of income that supports your aspirations of financial independence.

Credit: cnbc.com

Common misconceptions about financial independence

Financial independence means never working again

Being financially independent does not mean quitting your job and never working again. In essence, it’s about having autonomy over your time and pursuing fulfilling work. People may continue to work despite attaining financial independence if they love their profession. Being financially independent provides the freedom to decide one’s work schedule, whether part-time or volunteer.

Financial independence is only for the wealthy

Financial independence is not exclusive to the wealthy or those with high incomes, as popular belief holds. It primarily relies on efficient financial management and making prudent decisions with your finances, irrespective of your earnings. Individuals can achieve financial independence no matter what their income level is, through smart budgeting, savings, and investments.

Financial independence means sacrificing your quality of life

One misconception surrounding financial independence is that it demands a diminished quality of life and austere living. While exercising prudence in spending and prioritizing savings and investments is crucial, financial freedom does not equate to leading a deprived existence. It revolves around balancing enjoying the present moment and planning for the future. You can still indulge in experiences and purchases that bring you happiness while simultaneously working towards your financial independence objectives.

Resources and tools for achieving financial independence

The path to financial independence can present its challenges, but fear not, for many resources and strategies exist to support you in your journey. Below, you will find some invaluable tools that could prove advantageous:

Personal finance books and blogs

An abundance of personal finance literature and online content furnishes invaluable insights and strategies for attaining financial independence. Renowned books such as “The Millionaire Next Door” by Thomas J. Stanley and William D. Danko, “Your Money or Your Life” by Vicki Robin, and “Rich Dad Poor Dad” by Robert Kiyosaki are among the highly recommended reads. Furthermore, numerous personal finance blogs and websites furnish practical advice, helpful tips, and inspiring success stories from those who have accomplished financial independence.

Financial planning tools and software

Various financial planning software and tools are available to assist you in meticulously monitoring your expenses, effectively managing your budget, and devising plans for your financial future. Well-regarded options encompass Mint, Personal Capital, and YNAB (You Need a Budget). By automating your financial transactions, these tools can provide valuable insights into your spending patterns and facilitate accomplishing your financial objectives.

Financial advisors and coaches

Should you find yourself overwhelmed or uncertain about the path to financial independence, seeking guidance from a financial consultant or mentor may prove advantageous. These seasoned professionals offer tailored advice and strategies, taking into account your unique financial circumstances and aspirations. They can assist you in formulating a personalized plan, offer support and guidance, and ultimately steer you toward achieving financial independence.